Credit-card delinquencies are likely to become the next flashpoint in the credit crisis, though the impact on the overall economy won't be as severe as the housing slump, analysts believe.

|

|

AP

|

As the economy worsens and unemployment rises, more Americans are having trouble paying off their credit card balances. That has pushed up losses for credit card issuers, forcing them to tighten standards, which puts a further squeeze on cash-strapped consumers.

“After mortgages and home equity, credit cards are the next in line to feel the crunch,” says Marc DeCastro, an industry analyst with Financial Insights.

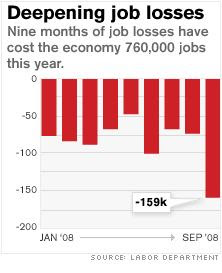

With job losses growing, credit cards delinquencies could rise to 7 percent by the first quarter of 2009, which would be a 20 year high, says Howard Shapiro, an industry analyst with Fox-Pitt Kelton.

And because consumers no longer have the equity in the house to fall back on, they're relying even more on credit cards to pay for living expenses.

“Now with their home equities getting shut off, people are going to start augmenting their income with their credit cards," DeCastro says. "They are going hit their limits and once they hit their limits, then they are probably going to walk away from their credit cards.”

Though consumer spending accounts for three-quarters of the US economy, the credit-card crunch isn't likely to be as big an economic blow as the housing crisis has been.

The reason is that credit card debt, while still large, is much smaller than the amount tied up in mortgages.

There is roughly $1 trillion of outstanding credit card debt—compared to $14 trillion worth of outstanding mortgages—and in the second quarter of 2008, $385 billion of this had been bundled into asset-based securities, according to the Securities Industry and Financial Markets Association

Another reason for the smaller fallout is that credit card issuers have been working over the past year to tighten standards and limit the damage.

“I don’t see the credit card industry facing the kind of stress that the mortgage industry has faced," says Shapiro. "They have had time to prepare, to tighten their underwriting standards which were not stretched to the same degree as they were in the mortgage industry."

Still, that doesn't mean the growing losses aren't going to hurt.

Credit card write-offs last year totaled $26.6 billion, and are on track to reach more than $41.4 billion this year. And that's just the beginning.

“We think 2009 is going to be a difficult year for the credit card industry," Shapiro says. "There’ll be higher charge offs, slower growth, people are cutting back on spending. That is going to mean pressure on earnings.”

Innovest Strategic Value Advisors forsees delinquencies rising through the next three quarters, peaking at 10 percent, with industry losses of close to $100 billion in 2009.

this is the beginning of the worse to come!